Company History and Business

JPMorgan Chase (JPM) is a global finacial service firm and banking institution operating in 50 countries. It is engaged in investment banking, financial sevices for consumers and small businesses, commercial banking, financial trancactions processing, asset management and private equity. It is a well-run moneymaking machine that =brought in $24 billion in revenues with $2.5 trillion in assets in the last quarter. With a outstanding CEO in Jamie Dimon who has lead the company through the financial crisis, the London Whale Losses, government investigations and a first first quarter 2014 loss, while still ensuring that the earning power of the firm isn't harmed or impaired by these problems.

Jamie Dimon has been the CEO of JPM since 2005 and Chairman of the Board since Dec. 31, 2006. Under his leadership, JPM has become the leading bank in domestic assets under management and market valuation, and the top credit card provider in the U.S. Dimon led JPM through the financial crisis and acquired Bear Stearns and Washington Mutual for pennies on the dollar, increasing JPM in size and scope. But the acquistion of Bear Stearns and Washington Mutual came with mortage-backed securities and potional government lawsuits by the Justice Department. Forseeing that JPM has injected $28 billion into its legal reserves, since the end of 2009. Starting with the London Whale losses, the bank has had the Justice Department investigate the company, resulting in penalties up to $20 billion, most of this happened within the past year.

Finances

Balance Sheet

2013 31/12

2012 31/12

2011 31/12

2010 31/12

| Total Current Assets | - | - | - | - |

| Total Assets | 2415689 | 2359141 | 2265792 | 2117605 |

| Cash & Due from Banks | 39771 | 53723 | 59602 | 27567 | | Other Earning Assets, Total | 1404299 | 1358307 | 1271811 | 1174042 | | Net Loans | 722154 | 711860 | 696111 | 660661 | | Property/Plant/Equipment, Total - Net | 14891 | 14519 | 14041 | 13355 | | Property/Plant/Equipment, Total - Gross | - | - | - | - | | Accumulated Depreciation, Total | - | - | - | - | | Goodwill, Net | 48081 | 48175 | 48188 | 48854 | | Intangibles, Net | 11232 | 9849 | 10430 | 17688 | | Long Term Investments | - | - | - | - | | Other Long Term Assets, Total | - | - | - | - | | Other Assets, Total | 175261 | 162708 | 165609 | 175438 |

|

| Total Current Liabilities | - | - | - | - |

| Total Liabilities | 2204511 | 2155072 | 2082219 | 1941499 |

| Accounts Payable | 194491 | 195240 | 202895 | 170330 | | Payable/Accrued | - | - | - | - | | Accrued Expenses | - | - | - | - | | Total Deposits | 1287765 | 1193593 | 1127806 | 930369 | | Other Bearing Liabilities, Total | - | - | - | - | | Total Short Term Borrowings | 267005 | 322106 | 287071 | 346332 | | Current Port. of LT Debt/Capital Leases | - | - | - | - | | Other Current liabilities, Total | - | - | - | - | | Total Long Term Debt | 317506 | 312215 | 322752 | 348302 | | Long Term Debt | 317506 | 312215 | 322752 | 348302 | | Capital Lease Obligations | - | - | - | - | | Total Debt | 584511 | 634321 | 609823 | 694634 | | Deferred Income Tax | - | - | - | - | | Minority Interest | - | - | - | - | | Other Liabilities, Total | 137744 | 131918 | 141695 | 146166 |

|

| Total Equity | 211178 | 204069 | 183573 | 176106 |

| Redeemable Preferred Stock, Total | - | - | - | - | | Preferred Stock - Non Redeemable, Net | 11158 | 9058 | 7800 | 7800 | | Common Stock, Total | 4105 | 4105 | 4105 | 4105 | | Additional Paid-In Capital | 93828 | 94604 | 95602 | 97415 | | Retained Earnings (Accumulated Deficit) | 115756 | 104223 | 88315 | 73998 | | Treasury Stock - Common | -14868 | -12023 | -13193 | -8213 | | ESOP Debt Guarantee | - | - | - | - | | Unrealized Gain (Loss) | 2798 | - | - | - | | Other Equity, Total | -1599 | 4102 | 944 | 1001 |

|

| Total Liabilities & Shareholders' Equity | 2415689 | 2359141 | 2265792 | 2117605 |

| Total Common Shares Outstanding | 3756.11 | 3803.95 | 3772.7 | 3910.3 |

| Total Preferred Shares Outstanding | 1.12 | 0.91 | 0.78 | 0.78 |

Income Statments

2013 31/12

2012 31/12

2011 31/12

2010 31/12

| Net Interest Income | 43319 | 44910 | 47689 | 51001 |

| Interest Income, Bank | 52996 | 56063 | 61293 | 63782 | | Total Interest Expense | 9677 | 11153 | 13604 | 12781 |

|

| Loan Loss Provision | 225 | 3385 | 7574 | 16639 |

| Net Interest Income After Loan Loss Provision | 43094 | 41525 | 40115 | 34362 |

| Non-Interest Income, Bank | 53287 | 52121 | 49545 | 51693 |

| Non-Interest Expense, Bank | -70467 | -64729 | -62911 | -61196 |

| Net Income Before Taxes | 25914 | 28917 | 26749 | 24859 |

| Provision for Income Taxes | 7991 | 7633 | 7773 | 7489 |

| Net Income After Taxes | 17923 | 21284 | 18976 | 17370 |

| Minority Interest | - | - | - | - |

| Equity In Affiliates | - | - | - | - |

| U.S GAAP Adjustment | - | - | - | - |

| Net Income Before Extraordinary Items | 17923 | 21284 | 18976 | 17370 |

| Total Extraordinary Items | - | - | - | - |

| Net Income | 17923 | 21284 | 18976 | 17370 |

| Total Adjustments to Net Income | -1330 | -1407 | -1408 | -1606 |

| Income Available to Common Excluding Extraordinary Items | 16593 | 19877 | 17568 | 15764 |

| Dilution Adjustment | - | - | - | - |

| Diluted Net Income | 16593 | 19877 | 17568 | 15764 |

| Diluted Weighted Average Shares | 3814.9 | 3822.2 | 3920.3 | 3976.9 |

| Diluted EPS Excluding Extraordinary Items | 4.35 | 5.2 | 4.48 | 3.96 |

| DPS - Common Stock Primary Issue | 1.36 | 1.2 | 1 | 0.2 |

| Diluted Normalized EPS | 6.27 | 5.95 | 5.37 | 5.26 |

For fiscal year 2013, the firm interest income decreased 5% to $53 billion and net interest income after loans after loan loss provision increased 4% to $43.09 billion. It earned $17 billion and had revenues of $96.billon for 2013. The company had legal expenses after taxes of $8.6 billion you the year. Total deposite of $453 billion up 10% from the prior year.

Financial Assets and Liquidity

| Ratio's | 2013 | 2011 |

| Debt to Equity | 1.68 | 1.62 |

| Total Equity to Total Assets | 0.09 | 0.09 |

| LT Debt to Total Assets | 0.12 | 0.12 |

| Tier 1 Capital | 11.9 | 12.6 |

| Tier 1 Common | 10.7 | 11.0 |

| Total Capital | 14.4 | 15.3 |

JPM Pretax Earnings

| | Net Common Income to Shareholders | Income Tax | Pretax Income |

| 1Q2013 | 6,121 | 2,553 | 8,684 |

| 2Q2013 | 6,101 | 2,802 | 8,903 |

| 3Q2013 | 5,346 | 2,278 | 7,624 |

| 4Q2013 | 5,322 | 1,258 | 6,580 |

JPM 12 month pretax earnings after adding back taxes paid is $31.8 billion. It trades at around $57 with 3.8 billion shares outstanding, giving JPM a market cap of $213 billion that a 14.6% pretax yield. Buying JPM stock at today's price will give a pretax return of 14.6%compaired to the 2.5% on treasury is pretty good.

What JP Morgan Considers Normal Range For Earnings

Under normalize environment JP Morgan net income of $24 billion with growth initiative that will allow the firm to earn more than $24 billion over time. With the growth initiative in place target for earnings of $27 billon. Using the $27.5 billion "normalize" figure with growth initiative and $1.3 billion in benefit from a 100 basis point increase in interest rates that would come to $39.3 billion pretax. Assuming a 30% tax rate and deducting $1.5 billion in preferred dividends thats leaves $37.8 billion. This implices a 17.8% pretax yield based on shares out standing and the current stock price.

Risk to JPM

There are risks to JPM mainly from the Department of Justice and its investigations of the bank. With $28 billion in its legal reserve it can weather the penalities from the Department of Justice. JPM has penalties totaling $20 billion from the Department of Justice. Department of Justice penalties broken down:

$2 billion civil penalties to settles DOJ claims under the Finacial Institutions Reform, Recovery, and Enforcement. $1.4 billion to settle federal and state securities claim by the National Credit Union Administration $515.4 million to federal and state securities claims by the Federal Deposit Insurance Corporation $4 billion to federal and stater securities claims by the Federal Housing Agency $298.8 million to claims by the state of California $19.7 million to claims by the state of Delaware $100 million to claims by the state of Illionois $34.4 million to claims by the state of Massachusetts $613.8 million to claims by the stae of New York

JPM said about $7 billion of its penalties were tax-deductable, because of these penalties it earnings fell flat for the four quarter. JPM still has legal risk, but there is little risk to its business model, and earning power.

JPM Valuation

The firm is selling for 13x its earnings, 2.5x free cash flow, and 1.00x book value which shows that the company isn't cheap, but it is selling below its intrinsic value based on its pretax earnings, free cash flow and book value. JPM offers a 14.6% pretax return plus it's worth $86/share base on 10x its pretax earnings. By using $37.8 billion pretax earning or $9.94 per share at 10x will give you a $99.40 per share value and a 17% pretax return. JPM will continue to grow its earnings and make more money on its loans as interest rate moves up. Compared to Wells Fargo which offers a 12.8% pretax return, you'll getting one the best managed banks in the world with a higher return. JPM didn't just survived the 2008 crisis it thrived on it, making the bank one of the most stable and sound banks in the world. If JP Morgan traded at the same price to free cash flow as Wells Fargo then the company would sell for $130.00 per share or at the same price to book value $95.04 per share. Based on all of this it is very clear that JP Morgan intrinsic value is $99.40 per share and offers a 17% pretax yield which make it a great Long-Term Play for potential investors.

http://files.shareholder.com/downloads/ONE/3120446062x0x742266/2bd13119-52d2-4d78-9d85-a433141c21ae/01-2013AR_FULL_09.pdf

http://files.shareholder.com/downloads/ONE/3120447064x0x652147/a734543b-03fa-468d-89b0-fa5a9b1d9e5f/JPMC_2012_AR.pdf

http://money.cnn.com/2014/04/11/investing/premarkets/

About the author:Cody Eustice

Visit Cody Eustice's Website

| Currently 5.00/512345 Rating: 5.0/5 (1 vote) | Voters: |

Subscribe via Email

Subscribe RSS Comments Please leave your comment:

More GuruFocus Links

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

RSS Feed  | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

MORE GURUFOCUS LINKS

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

| RSS Feed | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

JPM STOCK PRICE CHART

55.7 (1y: +14%) $(function(){var seriesOptions=[],yAxisOptions=[],name='JPM',display='';Highcharts.setOptions({global:{useUTC:true}});var d=new Date();$current_day=d.getDay();if($current_day==5||$current_day==0||$current_day==6){day=4;}else{day=7;} seriesOptions[0]={id:name,animation:false,color:'#4572A7',lineWidth:1,name:name.toUpperCase()+' stock price',threshold:null,data:[[1367211600000,48.92],[1367298000000,49.01],[1367384400000,48.01],[1367470800000,48.08],[1367557200000,47.57],[1367816400000,48.18],[1367902800000,49.14],[1367989200000,49.76],[1368075600000,49.04],[1368162000000,48.96],[1368421200000,49.67],[1368507600000,50.23],[1368594000000,51.09],[1368680400000,50.97],[1368766800000,52.3],[1369026000000,52.29],[1369112400000,53.02],[1369198800000,53.63],[1369285200000,53.35],[1369371600000,53.66],[1369717200000,54.6],[1369803600000,54.67],[1369890000000,55.62],[1369976400000,54.59],[1370235600000,54.49],[1370322000000,54.04],[1370408400000,53.03],[1370494800000,53.5],[1370581200000,54.27],[1370840400000,54.36],[1370926800000,53.49],[1371013200000,53.18],[1371099600000,54.17],[1371186000000,53.13],[1371445200000,53.85],[1371531600000,54.11],[1371618000000,53.55],[1371704400000,52.48],[1371790800000,51.96],[1372050000000,50.92],[1372136400000,52.08],[1372222800000,52.5],[1372309200000,53.15],[1372395600000,52.79],[1372654800000,52.49],[1372741200000,52.8],[1372827600000,52.77],[1373000400000,53.99],[1373259600000,54.7],[1373346000000,54.89],[1373432400000,54.83],[1373518800000,55.14],[1373605200000,54.97],[1373864400000,54.89],[1373950800000,55.01],[1374037200000,55.27],[1374123600000,56.37],[1374210000000,56.16],[1374469200000,56.56],[1374555600000,56.67],[1374642000000,56.63],[1374728400000,56.5],[1374814800000,56.05],[1375074000000,55.69],[1375160400000,55.33],[1375246800000,55.73],[1375333200000,56.54],[1375419600000,56.49],[1375678800000,56.1],[1375765200000,55.49],[1375851600000,55.3],[1375938000000,54.83],[1376024400000,54.52],[1376283600000,54.09],[1376370000000,54.29],[1376456400000,54.15],[1376542800000,53.29],[1376629200000,53.29],[1376888400000,51.83],[1376974800000,52.12],[1377061200000,51.63],[1377147600000,52.21],[1377234000000,52.32],[1377493200000,51.8],[1377579600000,50.6],[1377666000000,50.58],[1377752400000,50.7],[137783! 8800000,50.53],[1378184400000,51.13],[1378270800000,51.87],[1378357200000,52.11],[1378443600000,52.56],[1378702800000,52.86],[1378789200000,53.67],[1378875600000,53.26],[1378962000000,52.24],[1379048400000,52.59],[1379307600000,53.14],[1379394000000,53.09],[1379480400000,53.41],[1379566800000,52.75],[1379653200000,52.8],[1379912400000,51.46],[1379998800000,50.32],[1380085200000,51.7],[1380171600000,51.89],[1380258000000,52.24],[1380517200000,51.69],[1380603600000,51.96],[1380690000000,52.09],[1380776400000,51.94],[1380862800000,52.67],[1381122000000,51.83],[1381208400000,50.87],[1381294800000,50.75],[1381381200000,52.52],[1381467600000,52.51],[1381726800000,52.71],[1381813200000,52.31],[1381899600000,54],[1381986000000,54.21],[1382072400000,54.3],[1382331600000,54.27],[1382418000000,53.62],[1382504400000,52.75],[1382590800000,52.48],[1382677200000,52.77],[1382936400000,52.68],[1383022800000,52.73],[1383109200000,52.6],[1383195600000,51.54],[1383282000000,52.51],[1383544800000,52.04],[1383631200000,51.95],[1383717600000,52.1],[1383804000000,51.65],[1383890400000,53.96],[1384149600000,54.1],[1384236000000,53.97],[1384322400000,54.14],[1384408800000,54.4],[1384495200000,54.87],[1384754400000,55.74],[1384840800000,56.15],[1384927200000,56.1],[1385013600000,57.22],[1385100000000,57.46],[1385359200000,57.65],[1385445600000,57.17],[1385532000000,57.48],[1385704800000,57.22],[1385964000000,56.98],[1386050400000,56.86],[1386136800000,57.19],[1386223200000,55.82],[1386309600000,56.06],[1386568800000,56.51],[1386655200000,56.7],[1386741600000,56.07],[1386828000000,56.31],[1386914400000,56.17],[1387173600000,56.42],[1387260000000,55.72],[1387346400000,57.24],[1387432800000,57.23],[1387519200000,57.7],[1387778400000,58.24],[1387864800000,58.25],[1388037600000,58.2],[1388124000000,58.14],[1388383200000,57.95],[1388469600000,58.48],[1388642400000,58.21],[1388728800000,58.66],[1388988000000,59],[1389074400000,58.32],[1389160800000,58.87],[1389247200000,58.76],[1389333600000,58.49],[1389592800000,57.7],[1389679200000,57! .74],[138! 9765600000,59.49],[1389852000000,58.99],[1389938400000,58.11],[1390284000000,58.17],[1390370400000,57.59],[1390456800000,56.47],[1390543200000,55.09],[1390802400000,55.09],[1390888800000,55.74],[1390975200000,55.53],[1391061600000,56],[1391148000000,55.36],[1391407200000,54.31],[1391493600000,54.95],[1391580000000,55.21],[1391666400000,56.48],[1391752800000,56.62],[1392012000000,56.74],[1392098400000,57.43],[1392184800000,57.52],[1392271200000,58.03],[1392357600000,58.15],[1392703200000,58.49],[1392789600000,57.26],[1392876000000,57.58],[1392962400000,57.61],[1393221600000,58.03],[1393308000000,57.03],[1393394400000,56.75],[1393826400000,56.21],[1393912800000,57.26],[1393999200000,58.16],[1394085600000,58.9],[1394172000000,59.4],[1394427600000,59.2],[1394514000000,58.19],[1394600400000,57.92],[1394686800000,57.42],[1394773200000,56.8],[1395032400000,57.58],[1395118800000,58.06],[1395205200000,58.3],[1395291600000,60.11],[1395378000000,60.17],[1395637200000,61.07],[1395723600000,60.93],[1395810000000,59.9],[1395896400000,59.92],[1395982800000,60.04],[1396328400000,60.67],[1396414800000,60.48],[1396501200000,60.66],[1396587600000,59.81],[1396846800000,59],[1396933200000,58.85],[1397019600000,59.27],[1397106000000,57.4],[1397192400000,55.3],[1397451600000,54.96],[1397538000000,54.8],[1397624400000,55.26],[1397710800000,55.22],[1398056400000,55.03],[1398142800000,55.81],[1398229200000,56.05],[1398315600000,56.19],[1398402000000,55.7],[1398512137000,55.7],[1398512137000,55.7],[1398438094000,55.7]]};var reporting=$('#reporting');Highcharts.setOptions({lang:{rangeSelectorZoom:""}});var chart=new Highcharts.StockChart({chart:{renderTo:'container_chart',marginRight:20,borderRadius:0,events:{load:function(){var chart=this,axis=chart.xAxis[0],buttons=chart.rangeSelector.buttons;function reset_all_buttons(){$.each(chart.rangeSelector.buttons,function(index,value){value.setState(0);});series=chart.get('JPM');series.remove();} buttons[0].on('click',function(e){chart.showLoading();reset_all_buttons();chart.rangeSelector.buttons[0].setState(2);var extremes=axis.getExtremes();$.getJSON('/modules/chart/price_chart_json.php?symbol=JPM&ser=1d',function(data){if(data!=null){var extremes=axis.getExtremes();axis.setExtremes(data[1][0][0],data[1][data[1].length-1][0]);chart.addSeries({name:'JPM',id:'JPM',color:'#4572A7',data:data[1]});if(data[0][1]>=0){display=data[0][0]+" (1D: +"+data[0][1]+"%)";reporting.html(display);}else{display=data[0][0]+" (1D: "+data[0][1]+"%)";reporting.html(display);} chart.hideLoading();}});});buttons[1].on('click',function(e){chart.showLoading();reset_all_buttons();chart.rangeSelector.buttons[1].setState(2);var extremes=axis.getExtremes();$.getJSON('/modules/chart/price_chart_json.php?symbol=JPM&ser=5d',function(data){if(data!=null){var extremes=axis.getExtremes();axis.setExtremes(data[1][0][0],data[1][data[1].length-1][0]);chart.addSeries({name:'JPM',id:'JPM',color:'#4572

For those who may not know, each month we host a joint web chat for subscribers of The Energy Strategist (TES) and MLP Profits. The chat is conducted by Igor Greenwald, managing editor for TES and chief investment strategist for MLP Profits, and myself.

For those who may not know, each month we host a joint web chat for subscribers of The Energy Strategist (TES) and MLP Profits. The chat is conducted by Igor Greenwald, managing editor for TES and chief investment strategist for MLP Profits, and myself.

There is a certain sense of doom among income investors these days. It started with nerves over the Federal Reserve's tapering mishap and continues as the question of Chairman Ben Bernanke's succession hangs overhead. Ultimately income investors are fretting about what interest rates will look like once the Fed's manipulation is over.

There is a certain sense of doom among income investors these days. It started with nerves over the Federal Reserve's tapering mishap and continues as the question of Chairman Ben Bernanke's succession hangs overhead. Ultimately income investors are fretting about what interest rates will look like once the Fed's manipulation is over. This week in new hires, Cetera Financial Group welcomed Steve Dunlap; Jeff Pawliger was appointed as Janus' regional director for southern Florida, and PFM Group announced that Susan Musselman, Fred Eoff and Johanna Roodzant have joined with the acquisition of SDM Advisors.

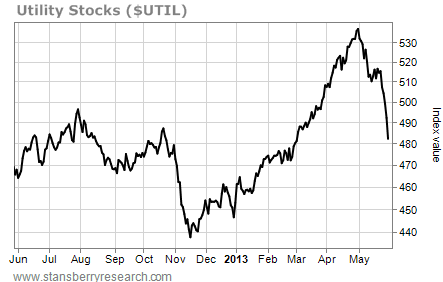

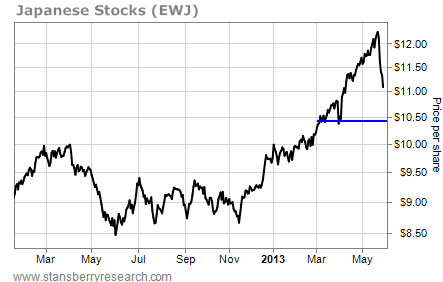

This week in new hires, Cetera Financial Group welcomed Steve Dunlap; Jeff Pawliger was appointed as Janus' regional director for southern Florida, and PFM Group announced that Susan Musselman, Fred Eoff and Johanna Roodzant have joined with the acquisition of SDM Advisors. So with this chart in mind – and with a profitable utility short sale under our belt – it's worthwhile to look for other parabolic moves in danger of breaking down. Here's what we found...

So with this chart in mind – and with a profitable utility short sale under our belt – it's worthwhile to look for other parabolic moves in danger of breaking down. Here's what we found...

– Jeff Clark

– Jeff Clark  NEW YORK (CNNMoney) Attention viewers in Grand Rapids, Des Moines and Augusta: it's almost safe to turn on the TV again.

NEW YORK (CNNMoney) Attention viewers in Grand Rapids, Des Moines and Augusta: it's almost safe to turn on the TV again.